Investors in Lowe's must

have felt they were living in some kind of parallel universe after the

company's excellent set of results were greeted by a 6.2% markdown on

the day. As ever, the usual knee-jerk response from journalists was to

seek out any possible negative in the company's report or commentary.

Lowe's results were a lot better than many made them out to be.

What really happened?

Perhaps the most relevant news on Lowe's results was the old news! The stock had such a major run up before the results that almost anything it said could somehow have been construed as a disappointment.

Not only had Lowe's share price increased by more than 50% in the last year, but it was also outperforming its main rival Home Depot .

Home Depot data by YCharts

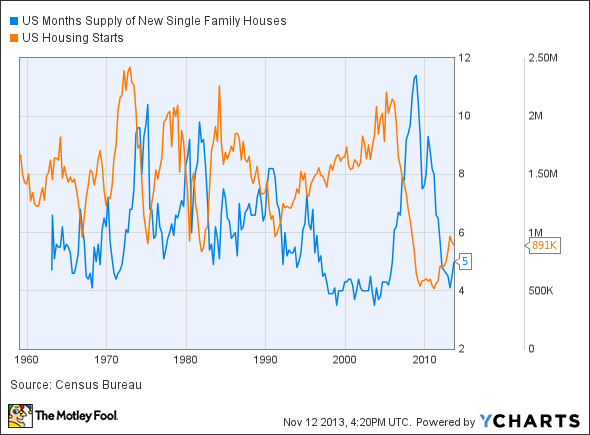

While it's true that economic commentators have

been becoming a little more cautious on the housing market due to higher

interest rates, you certainly wouldn't have noticed it from Lowe's

stock performance prior to the results.

Frankly, the sell-off after the results looked like

a correction of an overbought move and possibly some hedged pairs

trading going on with Lowe's versus Home Depot. In other words, traders

might have favored buying Home Depot and shorting Lowe's.

In reality, there were a number of positives from this report.

First, full-year earnings-per-share guidance was raised for the second time this year and now stands at $2.15.

Second, Lowe's management gave a positive industry

outlook. Management forecast that growth would persist in the fourth

quarter and went on to state "we expect further acceleration of industry

growth next year."

Third, it confirmed that its program of product

resets achieved around 100 basis points in gross-margin improvement once

the product lines "reached stabilization."The reset program is a

project to adjust the products the company sells in order to normalize

inventories across categories. Stabilization just refers to when it has

cleared out the old inventory.

Clearly, the project is working and Lowe's said

that only 66% of its business was stabilized by the end of the quarter.

Investors can look forward to margin improvements from the remaining 34%

in the future, as well as from the 20% of its business that hasn't even

been subject to resets yet.

Finally, the makeup of its sales is suggesting

industry strength. Lowe's declared that its Pro sales "continue to

outpace our [do-it-yourself] consumer." Indeed, only a day earlier, Home

Depot said a similar statement when its management declared "the

recovery of our pro business continues in the third quarter, our pro

business grew at a slightly faster pace than our consumer business."

Both companies see this as a sign of cyclical strength in housing.

In addition, Lowe's performed well with its large

product categories such as flooring, kitchens, and appliances. This is

in line with what appliance makers like Whirlpool are saying about the marketplace,

and customers' willingness to replace appliances that they bought 10

years ago at the height of the housing bubble. It also confirms the

positive outlook in the remodeling market index by the National

Association of Home Builders.

Weak spots?The

report was generally positive, but there were some points of caution.

While appliance sales were strong, the level of promotions was

significant enough to reduce the gross margin by 10 basis points. Such

developments will obviously concern Whirlpool investors, especially as

LG has now been added to Lowe's appliance offerings.

In addition, Lowe's has Samsung

and LG appliances highlighted on its floors. This is especially

relevant given that Whirlpool won an anti-dumping ruling against LG and

Samsung earlier this year.

The second possible sore point was that its

forecast of 5% full-year comparable- sales growth implies 4th quarter

comps growth of around 4%. As the graph shows, this is somewhat lower

than the last two quarters.

On the other hand, last year's fourth quarter was

positively affected by sales due to Hurricane Sandy. Furthermore, the

full-year forecast of 5% is an upgrade from the second quarter guidance

of 4.5% and first-quarter guidance of 3.5%. It's hardly bad news.

The bottom line

In conclusion, this wasn't a bad report at all. It's just that the stock had run up too much and investor expectations were probably too high Provided the housing market stays on track, the stock looks to be a good value on a P/E ratio of 17.8 times forward earnings as I write.

In conclusion, this wasn't a bad report at all. It's just that the stock had run up too much and investor expectations were probably too high Provided the housing market stays on track, the stock looks to be a good value on a P/E ratio of 17.8 times forward earnings as I write.

source: American Institute of Architects

source: American Institute of Architects